Linea Mercati Interview 12/15/25

December 16, 2025Peter’s 2026 economic forecast

December 17, 2025PETER CARDILLO

CHIEF MARKET ECONOMIST

INTRODUCTION

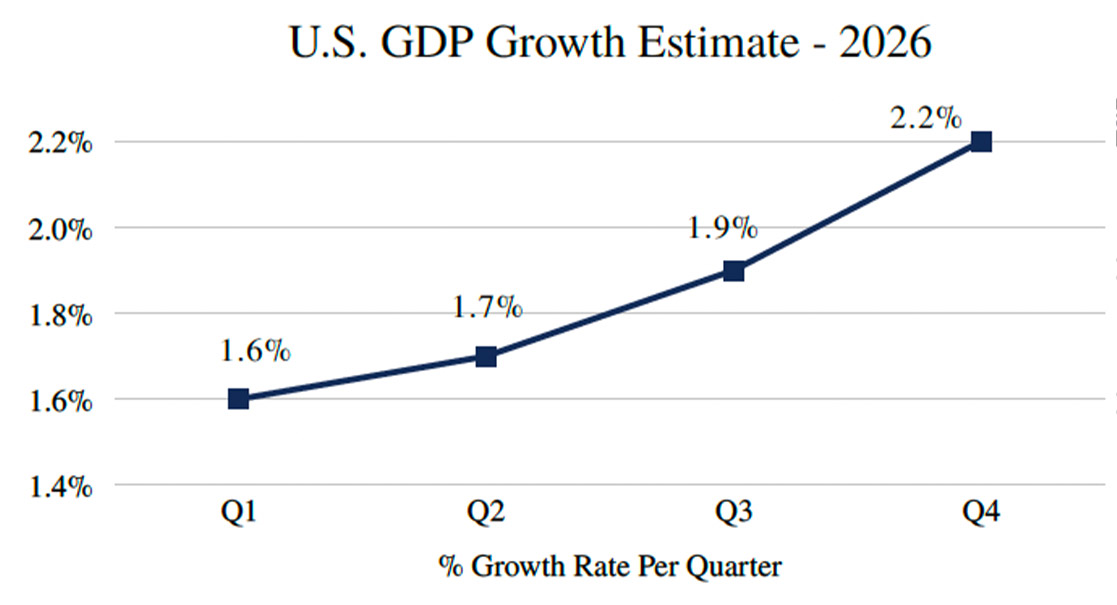

We expect the U.S. economy to remain weak through the first two quarters of 2026 as pressures in the labor market persist. Inflation is likely to stay sticky, with tariff-related cost impacts peaking in the first half of the year. Consumer confidence and spending should remain constrained in the first quarter, as the current K-type economic expansion continues to generate uneven outcomes across income groups. Conditions are expected to improve once tax benefits take effect in the second quarter, providing some support to household demand. For the full year, we project real GDP growth to average 1.85% per quarter in 2026.

HIGHLIGHTS

On the right, a visual for growth estimates per quarter for U.S. GDP shows growth rates strengthening throughout the year with the highest growth estimated to be at the end of 2026.

Other key highlights include:

- CAPEX growth seen at 9%

- Corporate Profits at 13%

EQUITIES

We expect equities to trend mostly higher in 2026, with a market correction of approximately 10% to 15% likely to begin in the latter part of the first quarter or early in the second quarter. This pullback is anticipated despite continued strong Q1 earnings and is driven primarily by overbought market conditions. We believe such a correction would help reset valuations and clear the path for a strong finish to the year, culminating in new all-time highs and an S&P 500 level of 7,300 or higher.

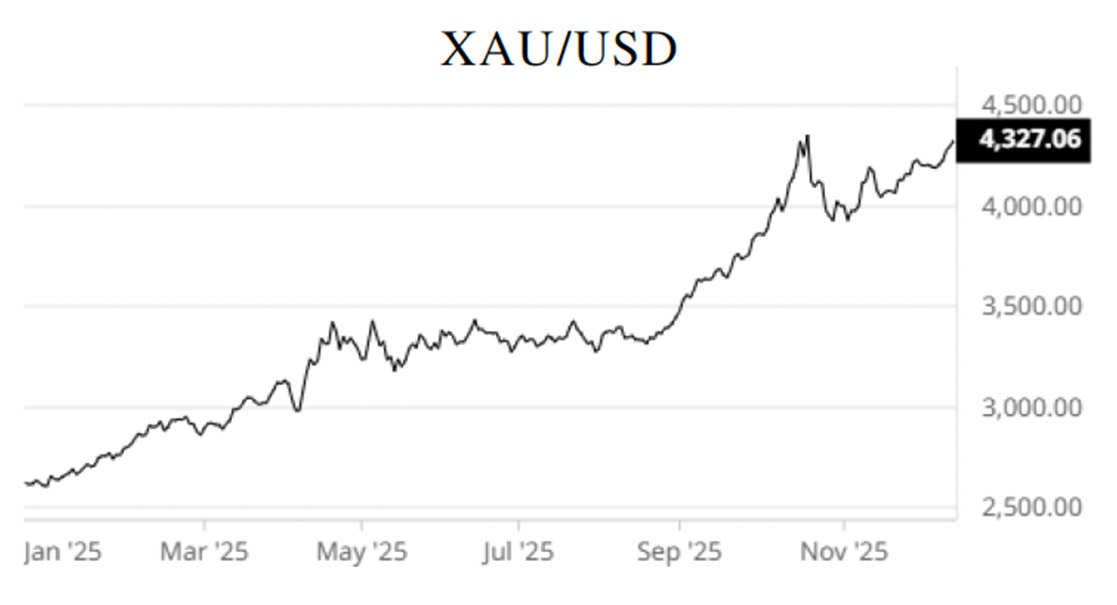

GOLD

We expect equities to trend mostly higher in 2026, with a market correction of approximately 10% to 15% likely to begin in the latter part of the first quarter or early in the second quarter. This pullback is anticipated despite continued strong Q1 earnings and is driven primarily by overbought market conditions. We believe such a correction would help reset valuations and clear the path for a strong finish to the year, culminating in new all-time highs and an S&P 500 level of 7,300 or higher.

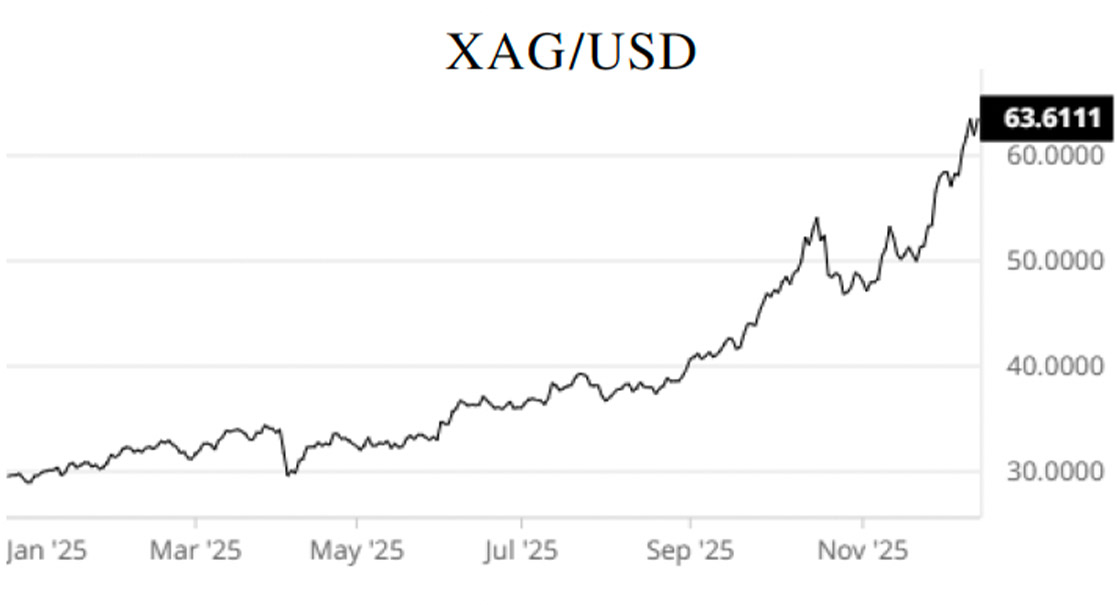

SILVER

We expect equities to trend mostly higher in 2026, with a market correction of approximately 10% to 15% likely to begin in the latter part of the first quarter or early in the second quarter. This pullback is anticipated despite continued strong Q1 earnings and is driven primarily by overbought market conditions. We believe such a correction would help reset valuations and clear the path for a strong finish to the year, culminating in new all-time highs and an S&P 500 level of 7,300 or higher.

FIXED INCOME

The bond market experienced relatively volatile trading in 2025, followed by a strong rally as the Fed embarked on easing monetary policy in the latter part of the year. Once again, uncertainties over tariffs and their negative impact on inflation weighed on yields, causing stress in the bond market. With inflation uncertainties persisting—particularly sticky tariff-related inflation—we expect yields to follow a similar trading pattern in 2026.

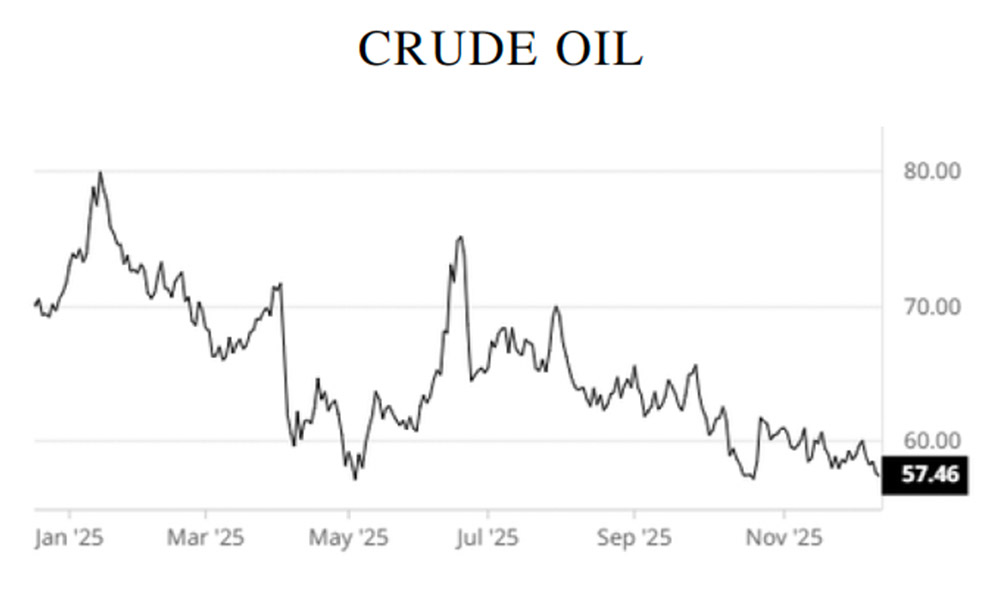

CRUDE OIL

Crude oil prices in 2025 remained mostly in a bearish trend as OPEC production stayed elevated and the U.S. continued to increase output to record levels. In addition, the present administration expanded offshore production as the Trump administration’s deregulation efforts supported further U.S. exploration. Demand factors were weak, largely due to uncertainties over the trade war, creating an imbalance between supply and demand. In 2026, we expect U.S. production to continue climbing, with both domestic and global demand rising modestly above 2025 levels. On the other hand, we see OPEC+ reining in production during the second quarter of 2026 to keep the market in balance. Decreases in OPEC+ production is likely to occur in the second and third quarters of 2026. In conclusion, we expect crude oil prices in 2026 to average around $67 per barrel.

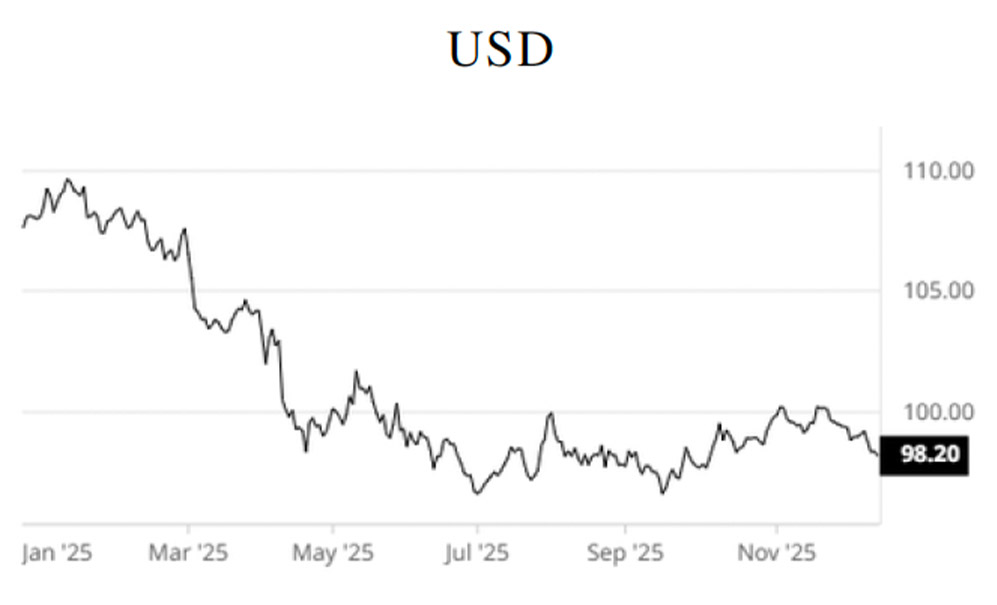

U.S. DOLLAR

The U.S. Dollar Index fell from its high point in 2025 before recovering in the latter part of the year. The ongoing trade war contributed to market uncertainties, while an easing of monetary policy narrowed interest-rate differentials, favoring other currencies. The unwinding of the carry trade versus the Japanese yen also added pressure to the U.S. dollar. In 2026, we see a narrowing of the trade deficit due in part to tariffs, which may provide some support for the world’s reserve currency. Nevertheless, the risk of a foreign-exchange–related crisis in 2026 remains elevated and could create periods of distress for the dollar. As a result, we believe the Dollar Index is likely to experience wider-than-usual swings as these factors continue to weigh on the market. We expect the Dollar Index to trade within a range of roughly 90 to 100 in 2026.

Disclosur

This report has been prepared as a matter of general information regarding market conditions, it is not to be a complete description of any security or company mentioned, and is not an offer to buy or sell any security. All facts and statistics are from sources believed reliable, are not guaranteed to accuracy. Transactions may be effected which are inconsistent with research reports. The views expressed herein accurately reflect personal views.

- This is not an offer to sell or solicitation to buy any security in any jurisdiction where such offer or solicitation would be illegal.

- Clients should consider whether any advice or recommendation is suitable for their particular circumstances and, if appropriate, seek professional advice, including legal and tax advice.

45 Broadway, 19th Floor New York, NY 1006 | Tel 212 293 0123 | 877 772 7818 | Fax 212 785 4565

www.spartancapital.com | Member of Finra | SIPC | MSRB Registered