Wind of panic on Wall Street: simple correction or prolonged depression?

January 24, 2022Wall Street’s Worst Week Since 2020

January 25, 2022Jan 24 – Welcome to the home for real-time coverage of markets brought to you by Reuters reporters. You can share your thoughts with us at [email protected]

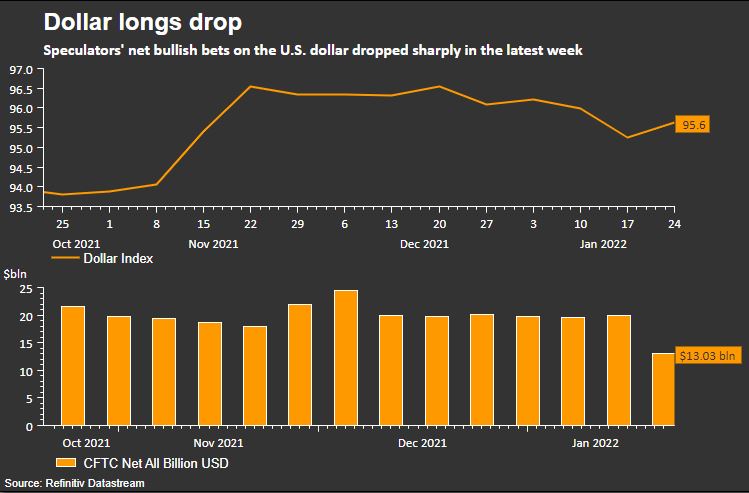

SHAKEOUT OF DOLLAR LONGS MAY BE BULLISH FOR GREENBACK (1345 EST/1845 GMT)

A large drop in speculative long dollar positions last week has resulted in the U.S. currency being less overbought, which may bode well for further gains as investors reestablish trades, according to ING.

The value of speculators’ net long dollar position against six major peers fell to $12.59 billion for the week ended Jan. 18, the lowest since mid-September, and down from $19.34 billion the previous week. according to calculations by Reuters and U.S. Commodity Futures Trading Commission data released on Friday. read more

Versus reported G10 currencies, dollar longs shrank by approximately 4% of open interest, moving close to its 5-year average, Francesco Pesole, FX strategist at ING said in a note on Monday.

“That corroborates our view that the dollar’s weakness at the start of the year was largely due to some position-squaring/profit-taking events around two major data releases (the nonfarm payrolls and the inflation report), rather than a structural shift away from bullish dollar sentiment,” Pesole said.

Now, “the more balanced positioning likely allowed some of those lost dollar longs to be built up again in the past week, as the dollar recovered across the board,” he added.

The greenback dropped against a basket of its peers to a two-month low of 94.63 on Jan. 14, before rebounding to 95.88 on Monday. It is down from a one-and-a-half-year high of 96.94 reached in November.

The dollar is expected to benefit as the Federal Reserve raises interest rates. The U.S. central bank is expected to hike in March, and increase rates four times in total this year. FEDWATCH

“Looking ahead, the lack of indication that the dollar net-long positioning is overstretched suggests that there is room for a further build-up in USD long positions into the start of Fed tightening cycle, which is historically a period where the greenback is well supported,” Pesole said.

(Karen Brettell)

****

WALL STREET BATTLES AGAINST BEARS AND CORRECTIONS (1309 EST/1809 GMT)

Wall Street appeared to be finding no other path but descent on Monday with all three of its major indexes firmly in deep red territory as investors watched over their shoulders at the Russia/Ukraine situation and just policy tightening details to look forward to at the Federal Reserve meeting this week.

Also in the mix was an earnings season that so far, has failed to impress with the bank stocks falling sharply and Netflix , the first of the major technology names bitterly disappointing investors last week.

A little over 15 minutes after the open, the S&P fell more than 10% below its Jan. 3 record close of 4,796.56 and since then just made the briefest forays above 4,316.904, the level at or below it would confirm a correction at the close.

This follows Nasdaq’s confirmation of a correction last week and the technology heavy index is last down more than 17% from its Nov. 19 record close. If Nasdaq closes at 12,845.9496 or below, this would confirm a bear market, which is a 20% decline from the most recent record.

With the S&P’s technology index (.SPLRCT), consumer discretionary (.SPLRCD) and communications services (.SPLRL) all falling more than 3% at one point it wasn’t hard to see why Nasdaq was in trouble.

The Russell 2000 (.RUT) fell as much as 20.9% below its most recent record, putting the small cap index on track to confirm a bear market, depending of course where it closes Monday.

While some market commentators blamed Fed nerves for the decline others were clearly anxious about international politics.

Peter Cardillo, chief market economist at Spartan Capital Securities talked about panic selling “based on a bad combination of factors.”

“The two factors that are really weighing on investor sentiment are the geopolitical situation as winds of war surface and fears that the Fed up may be overly aggressive this week,” he said.

Here is a snapshot where markets stand shortly after 1300 EST/1800 GMT:

(Sinéad Carew, Bansari Mayur Kamdar)

****

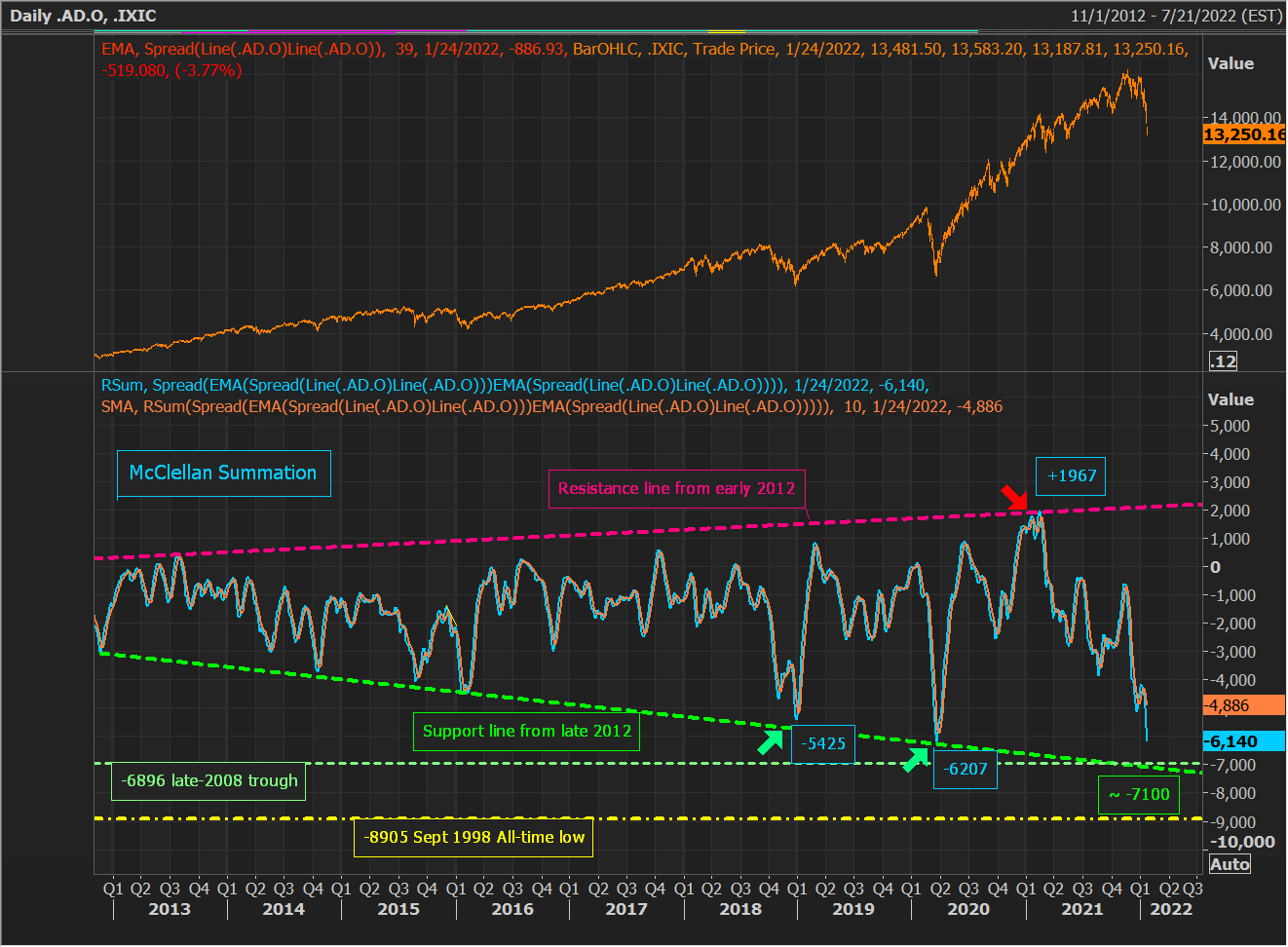

NASDAQ: SUMMARILY SMASHED (1203 EST/1703 GMT)

The Nasdaq Composite (.IXIC) is sliding around 4% on Monday, putting it down about 18% from its November-record close. read more

Amid the ongoing weakness, one measure of overall Nasdaq internal strength, the McClellan Oscillator (McOsc), which is based on advancing and declining issues, is plunging to -480. This is its lowest reading ever using Refinitiv data back to mid-1995.

With this, the McOsc is taking out the prior all-time low of -414 which was set during the market’s February/March 2020 pandemic crash.

Meanwhile, the McClellan Summation (McSum), which is a running sum of McOsc readings, is now hitting -6,140, which is nearly as low as its -6,207 print reached on March 23, 2020.

The McSum’s late-2008 trough was at -6,896 and its support line from late-2012, which contained its late-2018 and early-2020 weakness, now comes in around -7,100. The measure’s record low occurred in September 1998 at -8,905:

If the McSum takes out its 2020 trough, and maintains its current rate of descent, it could easily hit its 2008 low, and the support line by mid-week.

McSum troughs will not necessarily coincide with absolute market lows. For example, in 2008 the measure hit its low in late-November before converging bullishly into the market’s March 2009 low.

However, of note, the McSum did bottom just three trading days after the market’s December 24 2018 low, and in early 2020, it hit its low, on March 23, or the day the pandemic crash ended.

In any event, the current McOsc and McSum readings are a testament to just how weak this market has become.

(Terence Gabriel)

*****

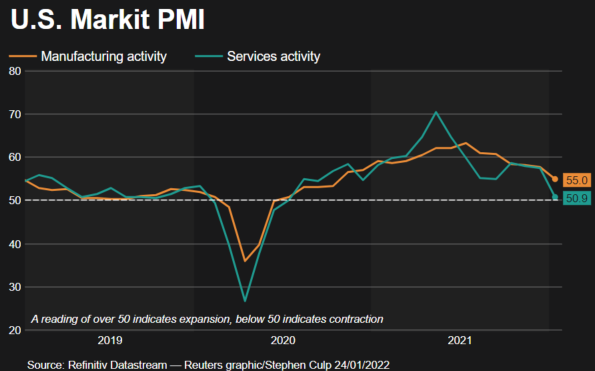

MARKIT PMI: OMICRON THROWS MONKEY WRENCH INTO U.S. BUSINESS ACTIVITY (1041 EST/1541 GMT)

The U.S. economy kicked off 2022 with a deceleration in business activity as it approached the hazardous turns and slippery conditions caused by Omicron.

Global financial information firm IHS Markit’s advance, “flash” purchasing managers’ index (PMI) for manufacturing (USMPMP=ECI) and services (USMPSP=ECI) sectors both fell more than expected, to respective readings of 55 and 50.9.

Combined, the indexes result in the lowest composite PMI print in 18 months.

A PMI reading over 50 signifies increased activity over the previous month.

Spiking infections due to the highly contagious Omicron COVID-variant are the main culprit for sending customer-facing services activity tumbling perilously close to contraction territory.

Output stalled as the new wave of COVID infections exacerbated existing supply and labor shortages.

“Soaring virus cases have brought the US economy to a near standstill at the start of the year, with businesses disrupted by worsening supply chain delays and staff shortages, with new restrictions to control the spread of Omicron adding to firms’ headwinds,” writes Chris Williamson, chief business economist at IHS Markit.

But the good news is that Omicron doesn’t appear to be hitting demand so much as adding complications to the already tangled supply chain.

“Output has been affected by Omicron much more than demand, with robust growth of new business inflows hinting that growth will pick up again once restrictions are relaxed.” Williamson adds.

Hinting at another silver lining, cost inflation pulled back to its slowest pace since March, while selling prices for goods and services registered the third-fastest rate on record, going back to October 2009.

Wall Street is sharply lower in morning trading extending its biggest weekly percentage plunge since March 2020, when measures to contain the new pandemic sent the economy into its steepest and most abrupt downturn in history.

The S&P 500 (.SPX) is on track to confirm a correction. It is last down 10.1% from its January 3 finish.

(Stephen Culp)

*****

WALL STREET TUMBLES AS WORRIES PILE ON (0944 EST/1444 GMT)

Wall Street’s three major indexes tumbled on Monday with Nasdaq down 2% leading the declines as the prospect of a Russian attack on Ukraine roiled global markets ahead of a Federal Reserve policy meeting later this week.

Also on investors minds was a sell off last week with the main indexes ending sharply lower Friday as Netflix shares set the tone with a plunge after a weak earnings report, capping the S&P 500 and Nasdaq’s biggest weekly percentage drops since the onset of the COVID-19 pandemic in March 2020. read more

NATO said on Monday it was putting forces on standby and reinforcing eastern Europe with more ships and fighter jets, in what Russia denounced as an escalation of tensions over Ukraine. President Joe Biden has begun considering options for boosting U.S. military assets in the region, senior administration officials said. read more

This week’s Fed meeting is expected to shed more light on the central bank’s plans for policy tightening including interest rate hikes.

The S&P’s 11 major sectors are in the red with defensives such as consumer staples (.SPLRCS) and utilities (.SPLRCU) losing the least ground, while growth stocks and cyclicals are among leading decliners with consumer discretionary (.SPLRCD) and financials (.SPSY) sliding.

Here is your opening snapshot:

(Sinéad Carew)

*****

DOW INDUSTRIALS: SLIP TURNS TO SLIDE (0900 EST/1400 GMT)

After ending January 4 at a record close of 36,799.65, the Dow Jones Industrial Average (.DJI) has now collapsed nearly 7% in just 12 trading days read more .

Much of this decline has come with a current six-day, near-6%, losing streak. And with CBT e-mini Dow futures reversing an overnight gain of 253 points, and now pointing to a loss of around 250 points at the open, the blue-chip average may threaten a seventh-straight day of losses.

The Dow last fell seven days in a row in February 2020, in the early stages of what would ultimately prove to be a 37% meltdown on a closing basis. The Dow last declined eight-straight days in June 2018.

Therefore, at least shorter-term, in terms of its streak, the DJI may be getting stretched to the downside.

Of note, the DJI ended Friday essentially right on its broken weekly log-scale resistance line from 1929, which has been acting as support since it was overwhelmed early last year. However, with opening weakness, the DJI will be below this line, which will ascend to around 34,300 this week:

Additional Dow support can be found at its mid-to-late 2021 troughs at 34,006, 33,613 and 33,271.

The 23.6% and 38.2% Fibonacci retracements of the entire March 2020 to January 2022 advance are found at 32,530 and 29,794. The Dow’s February 2020 peak was at 29,568.

In the event of sudden strength, which puts the DJI back over the line from 1929, it will still have work to do to repair its recent damage. This, given that its 40-week and 10-week moving averages are now resistance, and ended at 35,030 and 35,511 last Friday.

(Terence Gabriel)

*****

FOR MONDAY’S LIVE MARKETS’ POSTS PRIOR TO 0900 EST/1400 GMT – CLICK HERE: read more

Our Standards: The Thomson Reuters Trust Principles.