VIEW US November payrolls growth hurts case for early ’24 Fed cuts

December 8, 2023Wall Street fears the economy will slow down too much and end down

December 8, 2023PETER CARDILLO

CHIEF MARKET ECONOMIST

COMMENTARY

Our economic outlook for the first half of 2024 is for a very mild recession followed by a modest recovery inthe second half of the year. While we see inflation continuing to moderate, we do not expect the Fed’starget rate of 2% to be reached until the later part of 2025. We expect GDP growth in Q1 to be -0.1%, followedby flat to -0.1% in Q2. We expect a pickup in GDP in the third and fourth quarters around 1.8%.

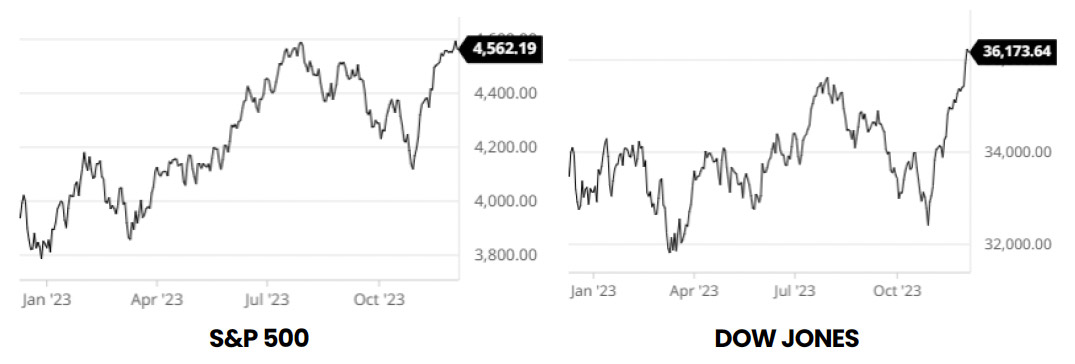

EQUITIES

We think overall market performance will be positive in 2024. While we anticipate a “January effect“ rally inthe first few months of the year, we do believe a pullback in the indices is not likely to be avoided in the laterpart of Q1. On the other hand, stocks in the second half of the year will likely outperform to the upside as thepresidential elections are traditionally positive for stocks.

GOLD

The price of the metal is poised to have anotherpositive year in 2024. Despite falling inflation,investors’ concern over heightened geopoliticalsituations, sub-modest global economic activity,falling yields, and a less robust dollar, will allcontinue to be factors for the metal to have anotherpositive year. We see the average price of gold inthe New Year fluctuating between the $2000 and$2300 level.

ENERGY

Oil prices are likely to cool off in the first half of 2024as demand continues to falter despite continuedefforts by OPEC+ to balance the demand factor.Obviously, geopolitical risk factors could step in theway for lower prices, however, barring any serious warfactors, we see crude oil in the first six-months of 2024averaging around the low $70 to mid-$60 range.

FOREIGN EXCHANGE

Although we expect the dollar to weaken from a veryrobust status, a meaningful correction of 10% or moreon the dollar index is not plausible. In fact, while theFeds are probably finished raising rates, we do notsee the Fed cutting rates until the later part of 2024.Indeed, a more pronounced recession than expectedcould force the Fed to take earlier action, however,while we continue to think a mild recession remains inthe forecast, the odds of inflation dropping to theFeds target rate of 2% in 2024 is feasible. Therefore,elevated yields, along with the concerns mentionedabove, will prevent the dollar from crashing. We seethe dollar index trading between the 95 – 104 level forin the first six months of the year.

FOREIGN EXCHANGE

Although we expect the dollar to weaken from a veryrobust status, a meaningful correction of 10% or moreon the dollar index is not plausible. In fact, while theFeds are probably finished raising rates, we do notsee the Fed cutting rates until the later part of 2024.Indeed, a more pronounced recession than expectedcould force the Fed to take earlier action, however,while we continue to think a mild recession remains inthe forecast, the odds of inflation dropping to theFeds target rate of 2% in 2024 is feasible. Therefore,elevated yields, along with the concerns mentionedabove, will prevent the dollar from crashing. We seethe dollar index trading between the 95 – 104 level forin the first six months of the year.

FIXED INCOME

We see yields hovering around present levels for agood part of the New Year before a big bond rallycommences in the later part of the year. We seethe 10-year TSY benchmark yield fluctuatingbetween 4.25% - 4.60% in the first six months of theyear.

Disclosure

This report has been prepared as a matter of general information regarding market conditions, it is not to be a complete description ofany security or company mentioned, and is not an offer to buy or sell any security. All facts and statistics are from sources believedreliable, are not guaranteed to accuracy. Transactions may be effected which are inconsistent with research reports. The viewsexpressed herein accurately reflect personal views.

- This is not an offer to sell or solicitation to buy any security in any jurisdiction where such offer or solicitation would be illegal.

- The Material provided here are for general informational purposes only and should not be construed as a recommendation or investment advice as the investments mentioned may not be suitable for or in the best interest of everyone.

45 Broadway, 19th Floor New York, NY 1006 | Tel 212 293 0123 | 877 772 7818 | Fax 212 785 4565

www.spartancapital.com | Member of Finra | SIPC | MSRB Registered

{kind=link}